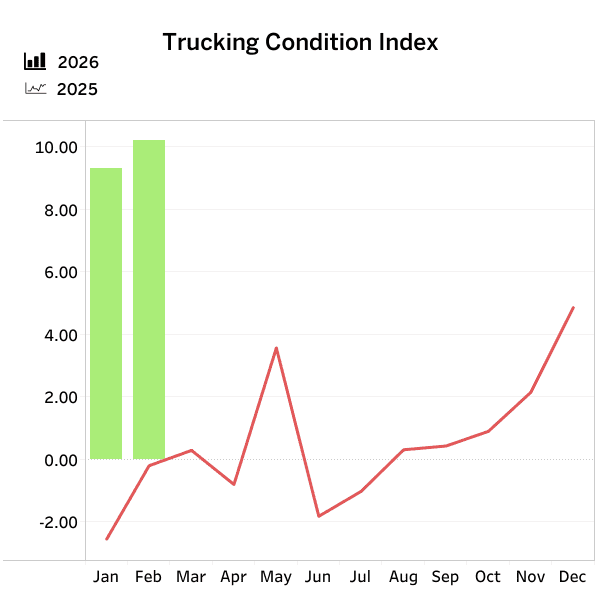

Freight Rates Push FTR's Trucking Conditions Index to 10.2, a Four-Year High

FTR's Trucking Conditions Index just hit its strongest reading since 2022, signaling a meaningful shift for carriers after years of soft freight. But fuel volatility threatens to cloud the picture in March.

TCI Climbs to 10.2 as Freight Rates Firm Up

FTR's Trucking Conditions Index reached 10.2 in February 2026, its highest reading in four years and a clear signal that the prolonged freight downturn is loosening its grip. The benchmark, which aggregates freight volumes, rates, fuel costs, and financing conditions into a single score, hadn't crossed double digits since the freight boom of 2022.

The driver this time is pricing power. Stronger freight rates -- not surging volumes -- did the heavy lifting in February, according to FTR's analysis reported by Heavy Duty Trucking. For fleet operators who have spent the better part of two years chasing thinner margins, the reading suggests rate negotiations heading into spring contract season may finally tilt back toward carriers.

Why Fuel Could Muddy the March Print

FTR is already tempering expectations for the next reading. The firm flagged fuel price volatility as a likely drag on March's TCI, a reminder that diesel swings can wipe out gains from rate improvements almost overnight.

For fleet managers, the practical takeaway is to watch fuel surcharge programs closely in the coming weeks. A strong TCI doesn't translate into operating margin if fuel costs outrun the recovery clauses in customer contracts. Fleets running tighter pass-through provisions or weekly resets will be better insulated than those still tied to monthly averages.

Capacity Is Tightening Underneath the Numbers

The TCI jump lines up with a quieter structural shift in the market. Carrier exits outpaced new entrants in Q3 2025, according to Trucking Dive, the kind of capacity attrition that typically precedes sustained rate strength. After two years in which weaker operators absorbed losses to keep trucks moving, the math finally caught up with a meaningful slice of the fleet.

That capacity tightening is the backdrop fleet leaders should keep in mind when reading any single month's index. One data point isn't a cycle, but a four-year high paired with shrinking carrier counts is a more durable signal than rates alone.

What to Watch Next

The March TCI release will be the first real test of whether February's reading marks a genuine inflection or a fuel-distorted blip. Beyond that, fleet operators should track three indicators: contract rate renewals in Q2, spot-to-contract spreads, and net carrier authority changes at FMCSA. If all three trend the same direction the TCI did in February, the recovery story gets a lot more credible.